Management of a company faced with an insolvency will have to make tough decisions to reduce debt, such as closing plants, selling off assets, and laying off employees. Even better, the company’s asset base consists wholly of tangible assets, which means that Solvents Co.’s ratio of debt to tangible assets is about one-seventh that of Liquids Inc. (approximately 13% vs. 91%). Overall, Solvents Co. is in a dangerous liquidity situation, but it has a comfortable debt position. Solvency defines whether a company can carry out their business operations or activities in the foreseeable (in future). Since it does not contain any of the elements included in the current ratio, the quick ratio is a more conservative method of measuring liquidity.

- Measuring and interpreting solvency in accounting involves analyzing a company’s financial statements to determine its ability to meet its long-term debt and understanding how it is performing financially in the long term.

- The debt to equity ratio compares the amount of debt outstanding to the amount of equity built up in a business.

- A rising debt-to-equity ratio implies higher interest expenses, and beyond a certain point, it may affect a company’s credit rating, making it more expensive to raise more debt.

- That means more cash coming in that you can use to pay down an excessive debt load.

Finance managers often look at their organization’s liquidity and solvency when assessing the ability to pay debts. Although both areas help strategize debt coverage, one focuses on addressing debts in the short-term through cash, while the other helps establish long-term financial stability. The first, as noted above, is a company’s cash or cash-equivalent assets it has on hand. These are assets that the business could reliably sell within a short period without taking a significant loss.

What is Liquidity?

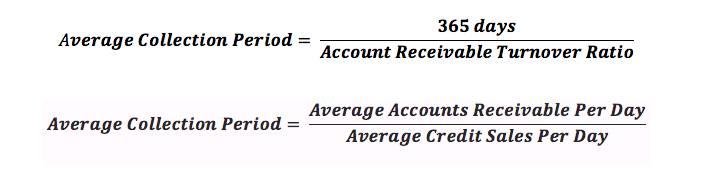

Excessive or inappropriate debt is dangerous and must be avoided through thoughtful debt management. If this ratio is above one it indicates that the company carries more liabilities than equity. The current economy has caused sales to slow dramatically and the time frame to collect Accounts Receivables to lengthen. Unlike sales, expenses seem to remain steady and while vendors are seeking cash more quickly, Accounts Payable payments tend to be deferred in order to conserve cash. What might appear to be a solid solvency ratio in one industry might be considered quite poor in another, so be sure to compare this information to the average for the relevant industry.

You can hope, but that’s not really a thing that should happen, especially if people know what’s going on. Well, in order to be back in the position of the George Bailey bank with respect to deposits (except 20% larger), you’ll need an extra $15 in fresh equity capital for each depositor, or another $1,500 total. Forecasts and budgets are key tools for successfully navigating this downturn. Best and worse case scenarios should be developed so that the company can prepare for either direction with confidence that enough cash is available for the continuance of operations.

A firm’s debt-to-equity ratio (D/E ratio) compares how much overall value, or equity, a company has compared to its overall debts. This is a measure of solvency, as it compares the company’s total value against its total liabilities. An especially high D/E ratio signals that it might have too much debt and might struggle to pays its bills; an especially low D/E ratio signals that it may not have invested enough in its own growth. This can signal a company that will stagnate and generate less value over the long run.

WHAT IS SOLVENCY RISK?

While cash-flow problems must be solved, investors don’t always need to write those companies off. As long as the underlying assets and value are strong, most solvent companies can solve cash-flow problems through short-term borrowing. Solvency vs liquidity is the difference between measuring a business’ ability to use current assets to meet its short-term obligations versus its long-term focus.

But you may be able to talk to existing investors into providing more funds if the terms are generous enough. The debt-to-equity ratio is one of the most fundamental solvency ratios. Since shareholder equity is the net value of a company after its assets are liquidated and its debts are paid, comparing debt to equity gives an excellent perspective on how leveraged up a company is. A company with a strong solvency position will have a healthy balance sheet with low debt and high liquidity ratios, indicating that it can pay its bills and maintain a strong financial position over time. The quick ratio measures the company’s capacity to meet short-term debt obligations with only quick assets, a subset of current assets.

- If this ratio is above one it indicates that the company carries more liabilities than equity.

- This situation can arise when a business has just received a large payment from a customer, but has such a poor sales backlog that it will not be able to continue generating positive cash flow over the long term.

- Solvency ratios, as a result, help you understand the overall efficiency of your business much better than liquidity ratios because liquidity of a business can change very frequently.

- It is the ability of a company or firm to meet current liabilities with current assets it has.

- Well, in order to be back in the position of the George Bailey bank with respect to deposits (except 20% larger), you’ll need an extra $15 in fresh equity capital for each depositor, or another $1,500 total.

- Understanding these terms is imperative since bankers, customers, owners, and lenders will use them to assess your company’s financial condition and decide whether or not they want to do business with you.

A higher ratio indicates a greater degree of leverage, and consequently, financial risk. Liquidity is a more short-term method of measuring your organization’s financial future. In the solvency vs liquidity debate, it is also a much more involving technique. Managing risks linked with liquidity is a critical part of a business-wide risk control system that should always be in place to help keep your operations running smoothly. The government is agreeing to pretend that this is more-secured than it actually is, since they’re treating treasuries that everyone knows are worth $85 (or whatever) are actually worth $100. If these treasuries were actually worth $100, the banks could just sell them for that price instead of needing loans.

Business Expenses: Definition, Types & Examples

These ratios also do not account for the presence of existing lines of credit that can be drawn down to access additional funding on short notice. When there is a large and mostly untapped line of credit, a business can easily pay its bills even when its solvency ratios are showing a bleak picture of its ability to pay. A high debt to equity ratio is especially dangerous when an organization’s cash flows are variable, as is the case with a start-up business or one that operates within a highly competitive industry. Conversely, a business may be able to comfortably maintain a high debt to equity ratio if it operates in a protected market where cash flows have historically been reliably consistent. Investors will often look for a cash flow-to-debt ratio of 66% or above. This ratio indicates that a company’s cash flow is two-thirds of its debt load.

Along with liquidity, solvency enables businesses to continue operating. The current ratio determines if your current assets are exceeding your current liabilities. It is used to tell if a company will be able to generate enough revenue to pay all its debts if they become due. It is used by dividing an organization’s current assets (cash, accounts receivable, inventory, and prepaid expenses) by its total current liabilities (both should be present on your balance sheet). Liquidity ratios provide indicators as to the company’s capacity to service debt in the short term while solvency ratios address the company’s ability to service long-term debt. Banks are especially interested in liquidity and solvency, showing the ability to pay rather than just the collateral securitizing the loan.

Cornerstone Research Experts in Focus: Andrea Eisfeldt – JD Supra

Cornerstone Research Experts in Focus: Andrea Eisfeldt.

Posted: Fri, 18 Aug 2023 07:00:00 GMT [source]

In other words, this measures debtors’ ability to pay their debts when they are owing. Quick assets are cash and cash convertibles only and do not include inventory and other receivables. It provides a more accurate picture of a company’s liquidity, as inventory can be harder to convert into cash quickly. A company that has the resources to pay all of its outstanding debts in full and on time is considered solvent.

Liquidity vs solvency: How do they affect cash flow?

A business that is completely insolvent is unable to pay its debts and will be forced into bankruptcy. Investors should examine all the financial statements of a company to make certain the business is solvent as well as profitable. There are key points that should be considered when using solvency and liquidity ratios.

In its practical application, this means the company could pay off all of its debt out of its cash flows in a year and a half. While it’s unlikely that a company would actually choose to do this, such a relatively high ratio means that the business has the ability to make significant strides in paying down its principal using ready cash. Solvency relative to liquidity is the distinction between the long-term focus between a company’s capacity to use its existing assets to deal with its short-term obligations. Solvency means the company’s long-term financial position, which means that the company has good net equity and the potential to meet long-term financial obligations. Liquidity ratios provide insight into a company’s short-term financial obligations, while solvency ratios provide a more comprehensive view of a company’s overall financial stability.

Key Differences Between Liquidity and Solvency

These ratios provide insight into a company’s financial stability and ability to pay off debts, bills, and other expenses, thereby hinting at the company’s creditworthiness. A fairly common measure related to solvency is the debt-to-equity ratio. If a company has more debt than equity, and this situation continues, they may find it difficult to service their debts and, eventually, end up insolvent – unable to meet their debt obligations.

An MBA builds upon existing knowledge and experience to improve finance professionals’ adaptability in an often-demanding work environment. These ratios help to determine the company’s ability to meet its current liabilities (short-term obligations) with current assets (cash and cash equivalents). Both liquidity and solvency help the investors to know whether the company is capable of covering its financial obligations or not, promptly.

How Do You Assess Solvency?

SmartAsset does not review the ongoing performance of any RIA/IAR, participate in the management of any user’s account by an RIA/IAR or provide advice regarding specific investments. Customers and vendors may be unwilling to do business with a company that has financial problems. In extreme cases, a business can be thrown into involuntary bankruptcy. However, it’s important to understand both these concepts as they deal with delays in paying liabilities which can cause serious problems for a business.

Adam received his master’s in economics from The New School for Social Research and his Ph.D. from the University of Wisconsin-Madison in sociology. He is a CFA charterholder as well as holding FINRA Series 7, 55 & 63 licenses. He currently researches and teaches economic sociology and the social studies of finance at the Hebrew University in Jerusalem. She is passionate about helping businesses overcome challenges that hamper their growth, which is why she is working at Monily to facilitate entrepreneurs to efficiently manage business finances and stay focused on growth. I did my math in zero-coupon bonds (pay $100 at maturity, yield is defined by discount to par) because it’s simpler and doesn’t change the analysis. My claim is not that the whole annual report will be read more closely for the rest of time; my specific claim is that the specific footnote about unrealized HTM losses will be read closely for the rest of time.